Is the American Dream Really a Debt Trap?

The conservative argument against consumerism

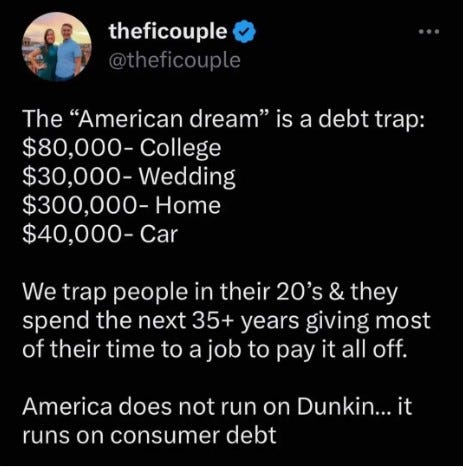

Courtesy of Aaron Clarey, I ran across this intriguing tweet. It makes a point worth responding to because it describes the thinking that dominates America’s dysfunctional culture:

First of all, America DOES run on consumer debt. The average American is 90k in debt and roughly 64% of Americans are living paycheck-to-paycheck. Shockingly, even 1/3 of Americans making $250,000 per year are living paycheck-to-paycheck. How is that possible, you may ask? Why is this happening?

Well, there are two answers.

The first requires us to look at the way our economic system encourages people to make poor spending decisions on an almost subconscious level.

Think about it like this.

When people earn money, they typically do one of three things with it. They spend it, they save it, or they invest it.

In a system where the money is “hard,” like the gold standard that the United States used to operate under, inflation tends to stay extremely low. In fact, between 1880 and 1910, inflation was only .1% per year. What that means is that if people earned a dollar back then, that dollar lost very little of its purchasing power over time to inflation. Because of that, people were heavily incentivized to save money over the long haul for important purchases, really good deals or to loan to other people.

Today, we have a “soft money” system. In other words, the paper in your pocket has almost no intrinsic value, nor could our government redeem it for hard assets if they were asked to do so. Worse yet, the government keeps printing more of it because who doesn’t want more “free money,” right? Except, of course, it’s not really “free.” The more money the government prints, the more inflation it creates and the less value each other piece of paper representing money has over the long term. So, for example, because of inflation, if you had saved $100,000 in cash thirty years ago and kept it under your mattress until today, the actual purchasing power of that money today would be less than 50% of what it was in 1993.

In other words, our current system disincentivizes saving. It creates a situation where if you have money (or credit), it can seem to make sense to spend it now rather than save it. It also can encourage people to take on much riskier investments. That’s because even a profitable investment with a low rate of return may be a loser over time because of inflation.

Saifedean Ammous talked about this subject in, The Fiat Standard: The Debt Slavery Alternative to Human Civilization:

Things claiming to be backed by gold would periodically fail, but the physical gold coin never failed. It very rarely depreciated, and when it did, it did not depreciate much or for long. This outlook that hard money encouraged existed in most of the world until the 1980s and 1990s, by which point fiat money, and the central-bank-led glut of fiat mining, had made debt inevitable and savings pointless for most people. Rather than save for major expenses, people now get into debt to pay for them, accruing a larger negative balance of fiat. People are born to families in debt and spend their entire lives in debt. Success consists of being able to secure ever-growing quantities of debt as you pass through the stages of life: a big college loan that allows you to get into the best paying job, whose salary will allow you a larger loan for a large house and another loan for a car. With more hard work at the company and dedication to its cause, you may succeed in getting an even larger negative balance of fiat for a bigger home and fancier car. Should you succeed even more and start your own business, you do not do it with your own accumulated capital, but rather with a bigger loan. The larger and the more successful the business, the more you are able to borrow. In sum, success in fiat means accumulating larger negative cash balances, and people live their entire lives stacking debt obligations upon themselves.

What he’s talking about there is the kind of consumerist mentality Chuck Palahniuk so artfully railed against in Fight Club. You may be thinking, “Wait a minute, that movie was about fighting, terrorists, insanity, and destroying the system, right?” Yes, but it also had gems like this in it:

You might think that a pro-capitalist conservative would be the last person you’d hear railing against consumerism, but if you’ve been reading Culturcidal for long, the one message that I have tried to get across over and over again is that our culture is broken and you won’t like where you end up if you just go with the flow.

What I am going to tell you is something so different from what you are hearing in popular culture, it may sound revolutionary.

I’m going to tell you that if you can get your future spouse to go along with it, there’s no way you should spend $30,000 on a wedding. Banking and investing $30,000 will do far more for any couple than some one-day ceremony ever could.

You also shouldn’t break the bank on a home. A lot of people – and the vast majority of people struggling to pay their bills – have more home than they need. They pay more for it than they should and pay more in insurance, taxes, and repairs than they would have otherwise. You may even want to at least consider moving to an area with cheaper housing. I’ve done that before (In fact, I’ve done everything I’m suggesting here at one time or am doing it, except for the wedding, since I’m not married).

As to cars, you don’t have to be one of the many people who get a brand, spanking new car every five years. Instead, you can get a used one, replace it every 10+ years, and save an enormous amount of money over the course of your life.

Additionally, you certainly don’t have to go $80,000 in debt for college. You can – and depending on the profession you’re going into; it might not even be a big deal for you. But, if you’re sweating paying it back, maybe you should be working. Joining the military to rack up money for college or just going to a cheaper school that isn’t going to break the bank.

We could go down the list of a lot of other smaller expenses, too. Bringing lunch from home instead of eating out for lunch. Skipping Starbucks, cable TV, expensive cell phones, designer clothes, and purses. Not dropping $500 on new video game systems and $50+ per game.

Some people read something like this and feel attacked, but it’s not about chastising anyone or guilt trips. It’s about looking at what most other people in America are doing, where their priorities are, and how it’s working out for them. Do you want to be economically average in America? Economically average in America is living paycheck-to-paycheck in a debt trap that it may take you decades to get out of if you ever do. What we’re talking about here is bucking the culture and attempting to go in a completely different direction:

If you can afford it and you want it, go for it! There’s nothing wrong with that. But, when it’s all said and done, it won’t be the “stuff” you acquire that makes your life meaningful or happy. When you’re 80, you’re not going to judge your life on how nice of a living room set you bought on credit when you were 30 or on how big the high-definition TV set you had for a few years happened to be. Those kinds of things aren’t worth spending years of your life stressing over money or wondering how you’re going to pay your bills. Do you want the American Dream? You can have it, but you’re going to be a lot happier if you chase it the right way.

The part about the expensive house cannot be overstressed! A large house means higher expenses as long as you own it and live in it. Property tax is where you find a genuine wealth tax (that you must pay every year), plus learn the hard truth that you are only leasing your house from the government- just see what happens when you don't pay that tax bill- "your" home will be auctioned off by the county, and the police will put you out of it and on the street. Thanks for reminding people of these realities that no one wants to advertise.